Long live uncertainty: the evolution of non-performance risk through the pandemic.

The coronavirus crisis was a great equaliser: the world is no longer split into those who know what force majeure is and those who don’t. Now, everyone knows.

In some ways force majeure clauses was the biggest party that never happened: companies either locked down together with their supply chains, or managed the crisis commercially, or swept disputes under the rug for litigation later on. Now, as lockdowns start to relax and businesses plan for a return to normality, is the topic going to die as quickly as it emerged?

We think not. Like the pandemic, there’s a long tail of uncertainty. We liked the way the next 1-3 years are laid out by Peter Schwartz in this scenario video from Salesforce (see 0:50 onwards). Let’s take a look at how force majeure and collateral contractual issues might play out through the three phases of the crisis. We’re going to do this by plotting the relevance of the issues along the crisis timeline.

(Note: the graphics in this article are based on a qualitative assessment based on what we’ve seen, read and heard. We have referred to supporting data where it is available).

Phase 0 - losing control

As supply chain disruption hit, we saw a spike of force majeure notices and non-performance. IACCM reported in April that, on a spot survey of 440 businesses, 60% were moderately or severely impacted by contract non-performance.

Businesses scrambled to understand what their contracts said. A small minority already had good contract systems in place so they could extract the information easily and react quickly. Others threw money at it with AI tools. Most muddled through it with a lot of effort and little structure. Not surprising that a poll by IACCM in April 2020 showed that 81% of member companies acknowledged that the pandemic accelerated the need to simplify and automate their contracting process.

Phase 1 - the hammer

As the lockdowns were enforced and countries engaged in the “hammer” phase, businesses did the same. Flattening the economic impact curve meant a spike of activity in managing contract and commercial issues with counterparties.

The real issue became the management of key supplier/customer relationships and agreeing interim arrangements to cover the lockdown period. We expect this is what procurement and customer success folk - and their lawyers - spent most of the spring doing.

Phase 2 - the dance

We’re now entering Phase 2. While the Phase 0 and 1 issues are falling away, we believe that new collateral issues will emerge and the overall the picture will start to get more complicated.

First, termination rights are kicking in. Typically 30-90 days after an ongoing force majeure event, one or more of the parties can terminate the contract. This is a new risk for suppliers and customers who are tied into a minimum term or exclusive arrangement and cannot exit at will. Customers who have inactive or underperforming suppliers now have a new way to exit the agreement with no consequences, and shift their business to alternative sources (perhaps the sources they’ve been relying on in the interim). Suppliers whose customers have been unable to take delivery (either due to lockdown or because the customer’s market tanked) can also shift their business elsewhere, leaving customers scrambling to fill the gap.

Second, as suppliers reduce or shut down operations to manage costs, their ability to respond to customer demand signals is going to be impacted. It’s a response management and cost issue for suppliers, and a supply continuity risk for customers, as respective needs and capabilities continue to be fragile.

Third, looking beyond the summer, Phase 2 may be an extended affair, with possible disruption and lockdowns in response to further waves of the virus (spikes in infections). This means non-performance issues coming to the fore again, this time more complicated because of two issues: (a) geographic variations and different lockdown policies will make the landscape more lumpy than in Phase 1; and (b) the pandemic is now nothing new. Not all supply chains will suffer equally - there’s likely to be more regional and seasonal variation. And those on the receiving end of non-performance will argue foreseeability: that repeated disruption should have been foreseen and preemptive steps taken. The first issue is a practical one, the second a legal one. Both will create more uncertainty than Phase 1 when everyone was in the same boat. Smart companies will seek to pre-empt the risk by accounting for it in their contracts and contingency plans.

Phases 2 & 3 - what is normal?

With the lockdown relaxing as we move through Phase 2, the big new issue is moving towards “normal”.

Again there are new commercial and legal uncertainties. How do you phase back in and what is “new normal” (presumably not exactly the same as pre-crisis normal)? How do you manage misalignments between customer demand and supply availability in this fragile period? Is there still a force majeure event that excuses performance? Are delays still excused if borders and supply chains are opening up? Is performance still impossible, or now just difficult, and how does that chime with the force majeure clause? Does the duty to mitigate have more teeth now, given that the parties have had months to adapt? What is going to be the impact of repeat lockdowns - is it all now foreseeable so force majeure cannot be relied on at all? Does the interim arrangement cover this phase or is there a need to renegotiate again?

Interpreting force majeure clauses and how they relate to facts on the ground is likely to be more tricky than in Phase 1 for these reasons.

Companies may need to renegotiate contracts across the board, not just to update the force majeure clause but to cover other differences and risks in the “new normal”. They need to know what’s in their agreement portfolio to prioritise and do it productively.

New risks

The uncertainty combined with ongoing economic hardship is going to bring new issues and exacerbate old ones. Except in the very best case scenario, as government support (furlough, social support, moratoria on redundancies) run out, the insolvencies will come. That’s a whole new battle front for those managing struggling supply chains and indebted customers.

The shape and size of this red curve is hard to predict - depending very much on the shape of the economic recovery - but it’s likely to be relevant into next year. Again, those who are prepared will waste less time and lose less money.

And of course there’s the risk of disputes and litigation, including unresolved Phase 1 issues catching up. If companies are more desperate, disputes will spike, though we hope we see more of the cooperation we saw in Phase 1.

The long view

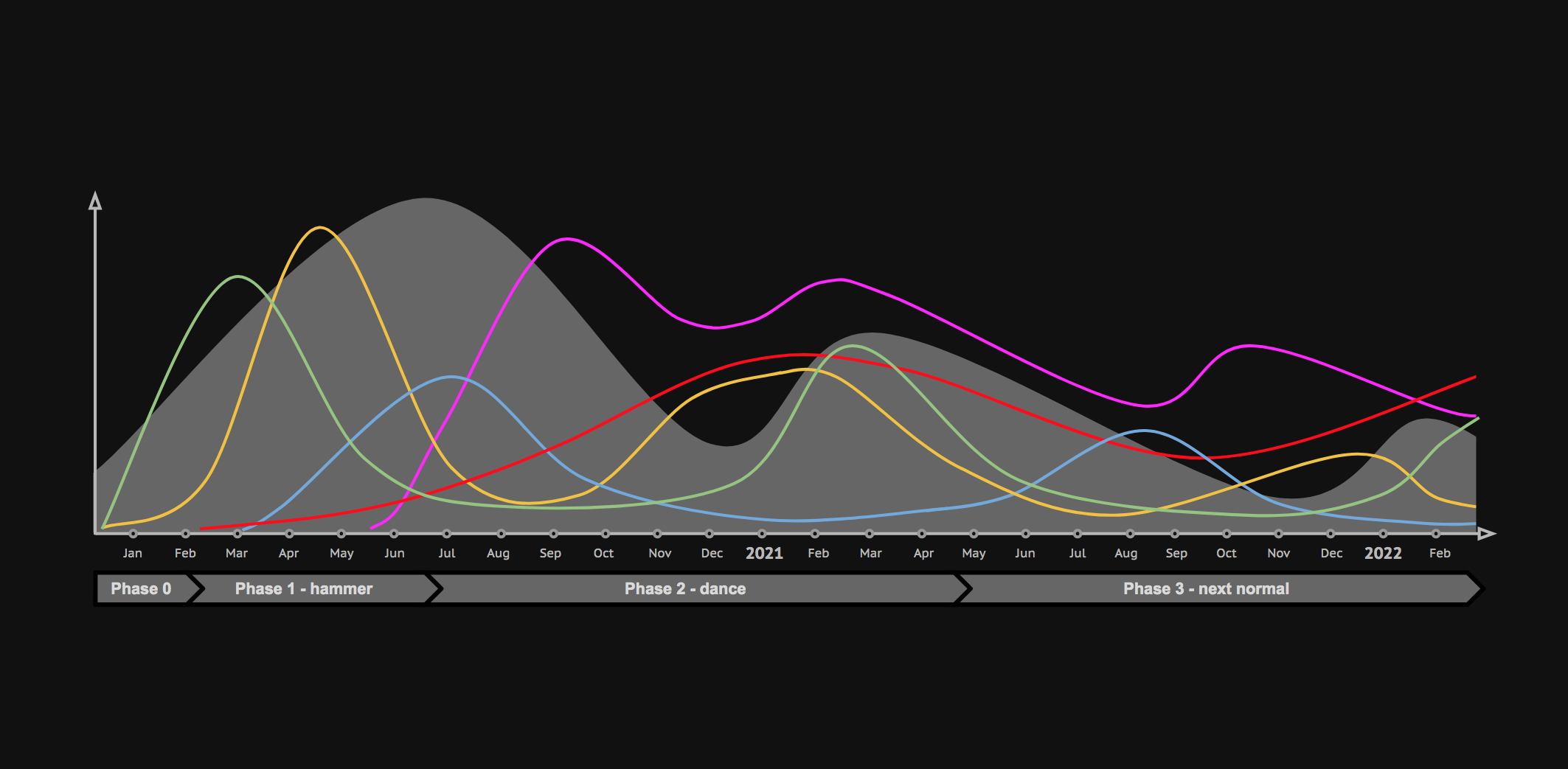

Let’s look beyond the next six months. The scenarios the experts are are showing us present a range of possible curves for how the pandemic - and the economic impact - could develop. The graphic below plots how the issues we’ve looked might look against scenario 3, the worst of the three medium-term scenarios presented by Peter Schwartz in his scenario video. (This is by no means a worst case scenario, since history and commentators warn us about bigger second waves at least in some regions).

Qualitative visualisation of contract non-performance issues through the phases of the coronavirus pandemic, based on Salesforce scenario 3.

Qualitative visualisation of contract non-performance issues through the phases of the coronavirus pandemic, based on Salesforce scenario 3.

In this scenario, force majeure, renegotiations and insolvencies will continue to be a feature throughout the path to the next normal, but with increasing uncertainty things get more lumpy regionally and as foreseeability and mitigation factors make it harder to rely on force majeure - even if there is real disruption driven by lockdowns. The work to manage that while transitioning customers and suppliers to the next normal will continue to challenge business functions and legal teams.

How can you increase certainty?

Be prepared, think ahead and resource for the required actions ahead of time. This includes understanding your contract portfolio and how your force majeure, termination and liability clauses play out in the different scenarios. We’ll cover how Majoto can help in an upcoming article. If you are looking for tools to help you meet this challenge, and can’t wait, get in touch.